Understanding How Repossession Works

Credit repair is fundamentally about managing three factors: accuracy of reports, payment behavior going forward, and aging of negative items. You can't change history, but you can correct inaccuracies, prove you're financially responsible now, and let time fade old damage. Most people dramatically underestimate what's possible because they think accurate negative information is permanent (it fades in power over time).

Start by checking your reports (free at AnnualCreditReport.com), identifying errors, and disputing inaccuracies in writing. While disputes process, focus on new credit behavior: pay every bill on time, reduce existing balances, avoid new hard inquiries. This dual approach of fixing reports while building positive history compounds over months.

Add yourself to positive accounts as an authorized user if possible. Family or friends with excellent credit and high limits can add you to their account. Their payment history and age show up on your report, boosting your score instantly by 50-100 points in many cases. There are no downsides if the primary account holder has perfect payment history and low utilization.

Becoming current on all accounts is critical. Stop the bleeding first. If you have delinquent accounts, get current immediately. One month of current payments doesn't erase the delinquency history, but it stops the daily credit score damage. After 3-6 months of current payments on previously delinquent accounts, you'll see significant score improvements.

Your Rights During a Repossession in Texas

Texas economy is diverse: oil and gas, tech, agriculture, manufacturing. Economic downturns in any sector hit credit scores of affected workers. 2015 energy crash, 2020 pandemic shutdowns, and regular business cycles all create credit casualties. What matters is recovery, and Texas law gives you tools to recover.

Texas has some of the best debtor protections in the country. Homestead exemption covers your residence up to certain values. Wage garnishment is capped at 25%. Non-discharge debts are limited. Chapter 7 bankruptcy is viable for many Texans. Understanding these laws and using them strategically gives you leverage in credit repairs and negotiations.

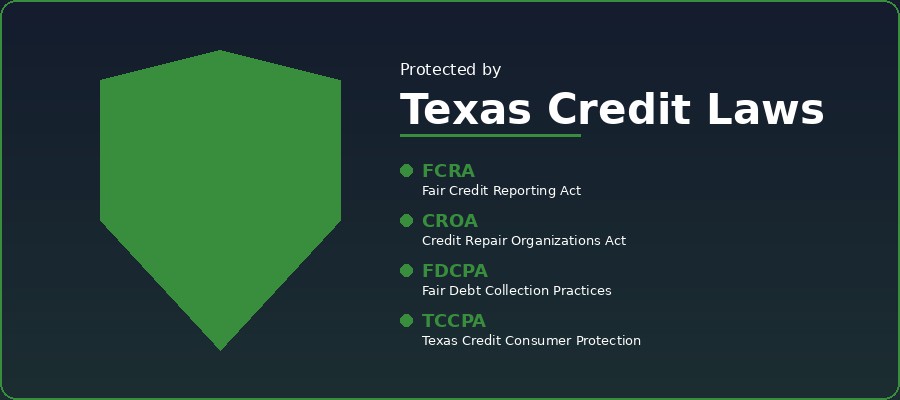

Credit repair in Texas involves knowing both federal law (FCRA, FDCPA, CROA) and Texas-specific rules (TCSOA, wage garnishment limits, homestead exemptions). A good Texas credit professional understands both and uses both to build the best strategy for your situation. DIY is possible but having local expertise helps.

Whether you're in San Antonio, Dallas, Houston, Austin, or a smaller Texas city, credit repair principles are the same: fix reports, build positive history, and let time heal. The details vary — Austin's tech economy is different from Houston's energy sector — but the core strategies work statewide. Reach out to 755CreditScore at 832-696-0755 for a free consultation.

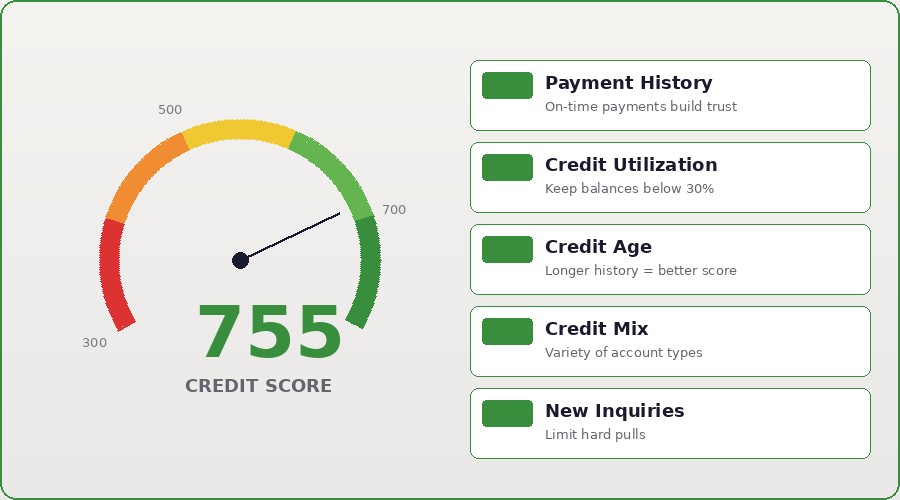

The Credit Score Impact of a Repo

Good credit repair isn't a single move — it's a comprehensive approach combining multiple strategies simultaneously. Check your reports for errors (dispute inaccuracies), reduce balances (payment history and utilization), become an authorized user on positive accounts (mix and age), stay current on all new payments (the most important factor), and wait for negative items to age (time heals credit wounds).

The timeline for visible results is 3-6 months if you're aggressive. If you dispute errors, you might see those removed in 30-90 days. If you pay down balances, your score improves within 1-2 billing cycles. If you get added as an authorized user, that score boost happens instantly. The compounding effect of multiple moves gives you 50-100 point improvements relatively quickly.

Realistic expectations: you can't remove accurate negative information, but you can dispute inaccurate items. You can't make old items disappear (but their impact fades over time). You can build a positive credit file starting today. Recovery from 450 credit to 700 credit typically takes 18-36 months with consistent action. It's not overnight, but it's absolutely achievable.

Work with credit professionals if DIY isn't moving the needle. Good credit repair companies combine dispute expertise, creditor negotiation skills, and strategic guidance. Legitimate companies charge ongoing fees (not upfront), give honest timelines, and focus on disputing inaccuracies and negotiating with creditors. The cost is worth it if it saves you months of effort and adds years to your credit recovery timeline.

What Happens After the Vehicle Is Sold

Credit repair is fundamentally about managing three factors: accuracy of reports, payment behavior going forward, and aging of negative items. You can't change history, but you can correct inaccuracies, prove you're financially responsible now, and let time fade old damage. Most people dramatically underestimate what's possible because they think accurate negative information is permanent (it fades in power over time).

Start by checking your reports (free at AnnualCreditReport.com), identifying errors, and disputing inaccuracies in writing. While disputes process, focus on new credit behavior: pay every bill on time, reduce existing balances, avoid new hard inquiries. This dual approach of fixing reports while building positive history compounds over months.

Add yourself to positive accounts as an authorized user if possible. Family or friends with excellent credit and high limits can add you to their account. Their payment history and age show up on your report, boosting your score instantly by 50-100 points in many cases. There are no downsides if the primary account holder has perfect payment history and low utilization.

Becoming current on all accounts is critical. Stop the bleeding first. If you have delinquent accounts, get current immediately. One month of current payments doesn't erase the delinquency history, but it stops the daily credit score damage. After 3-6 months of current payments on previously delinquent accounts, you'll see significant score improvements.

Rebuilding Credit After Repossession

Credit repair is fundamentally about managing three factors: accuracy of reports, payment behavior going forward, and aging of negative items. You can't change history, but you can correct inaccuracies, prove you're financially responsible now, and let time fade old damage. Most people dramatically underestimate what's possible because they think accurate negative information is permanent (it fades in power over time).

Start by checking your reports (free at AnnualCreditReport.com), identifying errors, and disputing inaccuracies in writing. While disputes process, focus on new credit behavior: pay every bill on time, reduce existing balances, avoid new hard inquiries. This dual approach of fixing reports while building positive history compounds over months.

Add yourself to positive accounts as an authorized user if possible. Family or friends with excellent credit and high limits can add you to their account. Their payment history and age show up on your report, boosting your score instantly by 50-100 points in many cases. There are no downsides if the primary account holder has perfect payment history and low utilization.

Becoming current on all accounts is critical. Stop the bleeding first. If you have delinquent accounts, get current immediately. One month of current payments doesn't erase the delinquency history, but it stops the daily credit score damage. After 3-6 months of current payments on previously delinquent accounts, you'll see significant score improvements.