Hard Inquiries vs Soft Inquiries

Every credit application creates a hard inquiry that briefly damages your score. It's a small hit — 5 to 10 points — but multiple inquiries in a short time add up. Someone applying for 3 credit cards in a month takes a bigger score hit than someone applying for 1. Plan your credit applications strategically to minimize inquiry damage.

Rate shopping window rules let you apply with multiple lenders without massive score damage. For auto loans, the window is typically 14-45 days (depending on the credit bureau). For mortgages, it's similar: applications within 14-45 days may count as one inquiry. This protection exists because lenders understand you'll shop around for rates — they'd rather you compare lenders than take the first offer you find.

Pre-approval inquiries are often soft inquiries (no score impact), while actual applications are hard inquiries. Ask creditors whether their pre-approval process includes a hard pull. If you're pre-approved and know you're not interested, decline it. You'll avoid the hard inquiry and the score impact. Only authorize hard inquiries when you're seriously considering applying.

The score damage from inquiries is temporary, but it's real. For 3-6 months after hard inquiries, your score is suppressed. After 12 months, the impact becomes minimal. After 24 months, the inquiry is invisible to credit scoring models. If you must apply for multiple loans, do it strategically: mortgage shopping in one window, auto shopping in another, debt consolidation months later. Spacing them out minimizes total damage.

How Many Points Does an Inquiry Cost?

Every credit application creates a hard inquiry that briefly damages your score. It's a small hit — 5 to 10 points — but multiple inquiries in a short time add up. Someone applying for 3 credit cards in a month takes a bigger score hit than someone applying for 1. Plan your credit applications strategically to minimize inquiry damage.

Rate shopping window rules let you apply with multiple lenders without massive score damage. For auto loans, the window is typically 14-45 days (depending on the credit bureau). For mortgages, it's similar: applications within 14-45 days may count as one inquiry. This protection exists because lenders understand you'll shop around for rates — they'd rather you compare lenders than take the first offer you find.

Pre-approval inquiries are often soft inquiries (no score impact), while actual applications are hard inquiries. Ask creditors whether their pre-approval process includes a hard pull. If you're pre-approved and know you're not interested, decline it. You'll avoid the hard inquiry and the score impact. Only authorize hard inquiries when you're seriously considering applying.

The score damage from inquiries is temporary, but it's real. For 3-6 months after hard inquiries, your score is suppressed. After 12 months, the impact becomes minimal. After 24 months, the inquiry is invisible to credit scoring models. If you must apply for multiple loans, do it strategically: mortgage shopping in one window, auto shopping in another, debt consolidation months later. Spacing them out minimizes total damage.

Rate Shopping: The Important Exception

Payday loans average 400% APR — that's insane compared to credit cards at 18-25% APR or personal loans at 8-15% APR. A $500 payday loan costs $100+ in fees alone, due in 2 weeks. If you can't pay, you roll it over and pay another $100+ in fees. What starts as a $500 problem becomes a $1,000 debt trap in 60 days.

Credit unions offer much better terms than payday lenders: loans at 8-15% APR with longer repayment periods. Most credit unions offer payday alternatives: short-term loans at reasonable rates designed specifically for people in emergency cash situations. You'll need membership (usually free or low cost), but the terms are infinitely better than payday shops.

Your credit score directly impacts the interest rate you qualify for. Someone with a 550 credit score might pay 18% APR on a car loan, while someone with a 750 score pays 3-5% APR. Over a 5-year car loan, that difference is tens of thousands of dollars. This is why credit repair isn't just about the score number — it's about the money you'll save on interest over decades.

Before taking on a loan, improve your credit if possible. Even a 50-point score improvement saves hundreds on interest. Wait 6 months if you need to: get on-time payments going, reduce credit card balances, dispute inaccuracies. The interest savings alone justify the wait. A $20,000 car loan at 8% versus 15% is $3,000+ in savings. Time spent improving credit pays direct financial dividends.

How to Manage and Reduce Inquiries

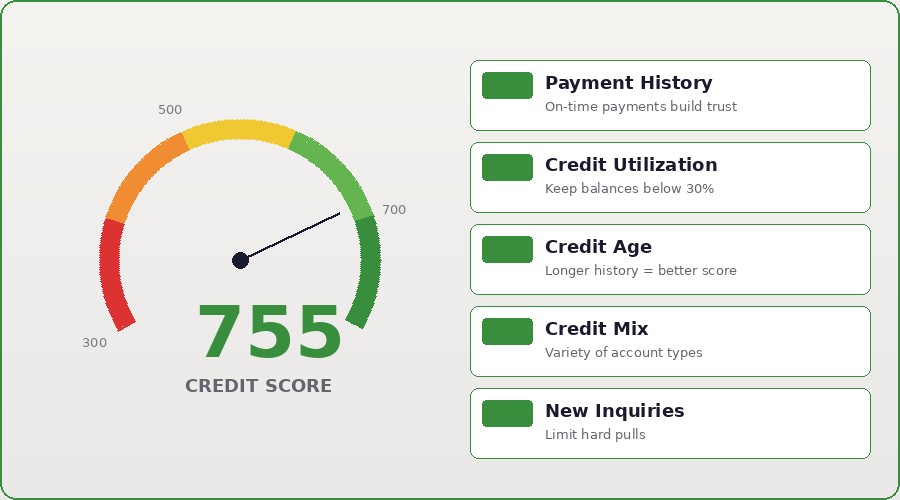

Hard inquiries drop your score 5 to 10 points each. Hard inquiries happen when you apply for credit — mortgage, auto loan, credit card. The inquiries stay on your report for 2 years but only impact your score for the first few months. Rate shopping for a mortgage or auto loan is protected: multiple inquiries within 14-45 days count as one inquiry, so comparing rates doesn't hammer your score if you do it efficiently.

Soft inquiries don't affect your score at all. These happen when you check your own credit, when existing creditors review your account, or when companies do pre-approval shopping (sending you 'prequalified' offers). You can't prevent soft inquiries, and they don't matter. Hard inquiries are the ones to watch.

If you're rate shopping, do it within a concentrated window — ideally 2 weeks or less, definitely within 45 days. The credit scoring models understand that rate shopping is normal and consolidate multiple inquiries as one when they're close together. Spread those applications out over 6 months, though, and each one individually hits your score.

Unauthorized inquiries can be disputed. If you see a hard inquiry you didn't authorize, contact the creditor and ask them to remove it. If they won't, send a written dispute to the credit bureau. You need to prove you didn't authorize it, but identity theft can cause unauthorized inquiries. Once removed, those 5-10 points come back to your score.

Get Unauthorized Inquiries Removed

Every credit application creates a hard inquiry that briefly damages your score. It's a small hit — 5 to 10 points — but multiple inquiries in a short time add up. Someone applying for 3 credit cards in a month takes a bigger score hit than someone applying for 1. Plan your credit applications strategically to minimize inquiry damage.

Rate shopping window rules let you apply with multiple lenders without massive score damage. For auto loans, the window is typically 14-45 days (depending on the credit bureau). For mortgages, it's similar: applications within 14-45 days may count as one inquiry. This protection exists because lenders understand you'll shop around for rates — they'd rather you compare lenders than take the first offer you find.

Pre-approval inquiries are often soft inquiries (no score impact), while actual applications are hard inquiries. Ask creditors whether their pre-approval process includes a hard pull. If you're pre-approved and know you're not interested, decline it. You'll avoid the hard inquiry and the score impact. Only authorize hard inquiries when you're seriously considering applying.

The score damage from inquiries is temporary, but it's real. For 3-6 months after hard inquiries, your score is suppressed. After 12 months, the impact becomes minimal. After 24 months, the inquiry is invisible to credit scoring models. If you must apply for multiple loans, do it strategically: mortgage shopping in one window, auto shopping in another, debt consolidation months later. Spacing them out minimizes total damage.