How Foreclosure Works in Texas

Texas uses non-judicial foreclosure, which moves faster than judicial states — sometimes as fast as 21 days from notice to sale. The lender doesn't need court permission; they just follow state law procedures and can sell your house on the first Tuesday of the month. This speed is a disadvantage for you, so understanding your options early is critical.

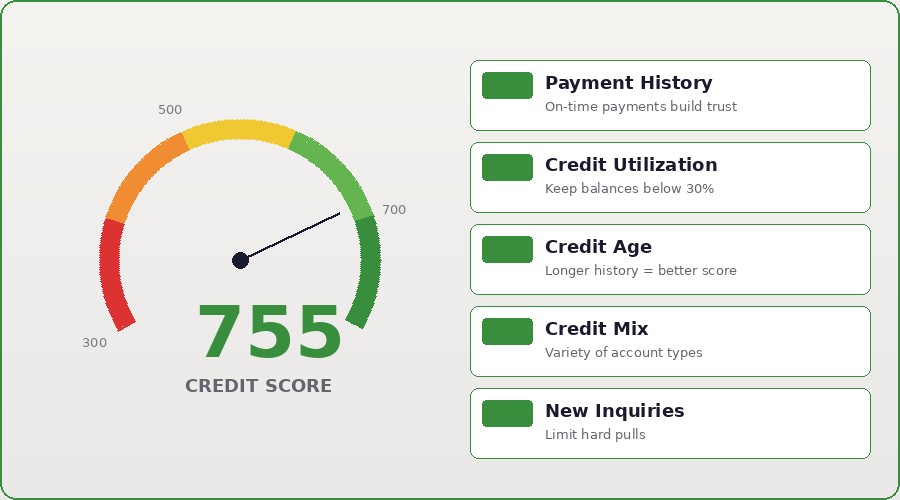

The score damage from a foreclosure is brutal: 100 to 160 points, depending on your starting score and how long the default lasted. A foreclosure stays on your report for 7 years, but similar to bankruptcy, you can rebuild faster than people expect. Most folks get back to a 650-700 score within 2-3 years if they take the right steps afterward.

Before a foreclosure completes, explore a deed-in-lieu. Contact your lender and propose transferring the deed directly to them instead of going through the sale process. It stops the foreclosure, you avoid the public sale, and you still lose the house but avoid some of the public record damage. Lenders don't always accept these, but it's worth asking.

A short sale is another option: sell the house for less than you owe and have the lender forgive the difference. This looks better on your credit than a foreclosure (though still negative), and you maintain some control over timing and buyer. The trade-off: it takes months to negotiate and requires the lender's approval. But it's worth exploring if you have equity cushion or time.

Warning Signs You're Heading Toward Foreclosure

Texas uses non-judicial foreclosure, which moves faster than judicial states — sometimes as fast as 21 days from notice to sale. The lender doesn't need court permission; they just follow state law procedures and can sell your house on the first Tuesday of the month. This speed is a disadvantage for you, so understanding your options early is critical.

The score damage from a foreclosure is brutal: 100 to 160 points, depending on your starting score and how long the default lasted. A foreclosure stays on your report for 7 years, but similar to bankruptcy, you can rebuild faster than people expect. Most folks get back to a 650-700 score within 2-3 years if they take the right steps afterward.

Before a foreclosure completes, explore a deed-in-lieu. Contact your lender and propose transferring the deed directly to them instead of going through the sale process. It stops the foreclosure, you avoid the public sale, and you still lose the house but avoid some of the public record damage. Lenders don't always accept these, but it's worth asking.

A short sale is another option: sell the house for less than you owe and have the lender forgive the difference. This looks better on your credit than a foreclosure (though still negative), and you maintain some control over timing and buyer. The trade-off: it takes months to negotiate and requires the lender's approval. But it's worth exploring if you have equity cushion or time.

Options to Avoid Foreclosure

The foreclosure process in Texas starts with a breach notice, then proceeds to sale without court involvement. Most sales happen on the first Tuesday of each month at the county courthouse. You have minimal time to respond — typically 21-30 days before the sale. The speed is designed to favor the lender, so knowing your options and acting fast matters.

Your credit score takes a massive hit from a foreclosure because it signals you couldn't pay your most important obligation — the mortgage. Lenders view this as maximum risk. That said, most foreclosures are 5-7 years old by the time borrowers apply for new mortgages, and if they've built perfect credit since then, many lenders will approve them.

Texas homestead laws protect some equity even in foreclosure. If the property is your primary residence, certain equity may be protected from judgment creditors post-sale. This doesn't stop the foreclosure itself, but it can protect you from a deficiency judgment (where the lender sues for the difference between sale price and balance owed).

Rebuilding after foreclosure involves secured cards, becoming an authorized user on positive accounts, and time. After 3 years with perfect credit history post-foreclosure, you're a viable mortgage candidate for many lenders. FHA mortgages are available after 3 years of foreclosure with strong recent credit. Conventional loans require 5-7 years. The timeline is long, but recovery is possible.

The Credit Score Impact of Foreclosure

Texas uses non-judicial foreclosure, which moves faster than judicial states — sometimes as fast as 21 days from notice to sale. The lender doesn't need court permission; they just follow state law procedures and can sell your house on the first Tuesday of the month. This speed is a disadvantage for you, so understanding your options early is critical.

The score damage from a foreclosure is brutal: 100 to 160 points, depending on your starting score and how long the default lasted. A foreclosure stays on your report for 7 years, but similar to bankruptcy, you can rebuild faster than people expect. Most folks get back to a 650-700 score within 2-3 years if they take the right steps afterward.

Before a foreclosure completes, explore a deed-in-lieu. Contact your lender and propose transferring the deed directly to them instead of going through the sale process. It stops the foreclosure, you avoid the public sale, and you still lose the house but avoid some of the public record damage. Lenders don't always accept these, but it's worth asking.

A short sale is another option: sell the house for less than you owe and have the lender forgive the difference. This looks better on your credit than a foreclosure (though still negative), and you maintain some control over timing and buyer. The trade-off: it takes months to negotiate and requires the lender's approval. But it's worth exploring if you have equity cushion or time.

Rebuilding Credit After Foreclosure with 755CreditScore

Texas uses non-judicial foreclosure, which moves faster than judicial states — sometimes as fast as 21 days from notice to sale. The lender doesn't need court permission; they just follow state law procedures and can sell your house on the first Tuesday of the month. This speed is a disadvantage for you, so understanding your options early is critical.

The score damage from a foreclosure is brutal: 100 to 160 points, depending on your starting score and how long the default lasted. A foreclosure stays on your report for 7 years, but similar to bankruptcy, you can rebuild faster than people expect. Most folks get back to a 650-700 score within 2-3 years if they take the right steps afterward.

Before a foreclosure completes, explore a deed-in-lieu. Contact your lender and propose transferring the deed directly to them instead of going through the sale process. It stops the foreclosure, you avoid the public sale, and you still lose the house but avoid some of the public record damage. Lenders don't always accept these, but it's worth asking.

A short sale is another option: sell the house for less than you owe and have the lender forgive the difference. This looks better on your credit than a foreclosure (though still negative), and you maintain some control over timing and buyer. The trade-off: it takes months to negotiate and requires the lender's approval. But it's worth exploring if you have equity cushion or time.