Understanding Houston's Credit Landscape

Houston is one of America's most diverse and rapidly growing cities, which means credit issues are everywhere — and solutions exist everywhere too. Whether you're dealing with job loss from industry downturns, medical debt from an unexpected health crisis, or just lifestyle creep from Houston's cost of living, credit repair is achievable.

The Houston metro is spreading outward fast: Pearland, Katy, Sugarland, and Woodlands are booming with young professionals and families. These suburbs have higher cost of living than inner Houston, which strains credit. If you're buying a house in these areas, having 650+ credit saves tens of thousands on mortgage rates alone.

Texas homestead exemption protects Houston homeowners in bankruptcy and judgment situations — that's a huge advantage many states don't have. If you're a homeowner struggling with debt, you might have more protection than you realize. Exploring options like Chapter 13 bankruptcy can actually let you keep your house while restructuring other debts.

Houston's culture is forward-focused, not backward-focused. A charge-off from 2019 is history. Bad credit from a 2020 business failure doesn't define you in 2024. Build your credit now with perfect on-time payments, and lenders evaluate you on current behavior, not 5-year-old mistakes. Call 755CreditScore today for a free consultation on rebuilding in Houston.

Step 1: Review Your Credit Reports

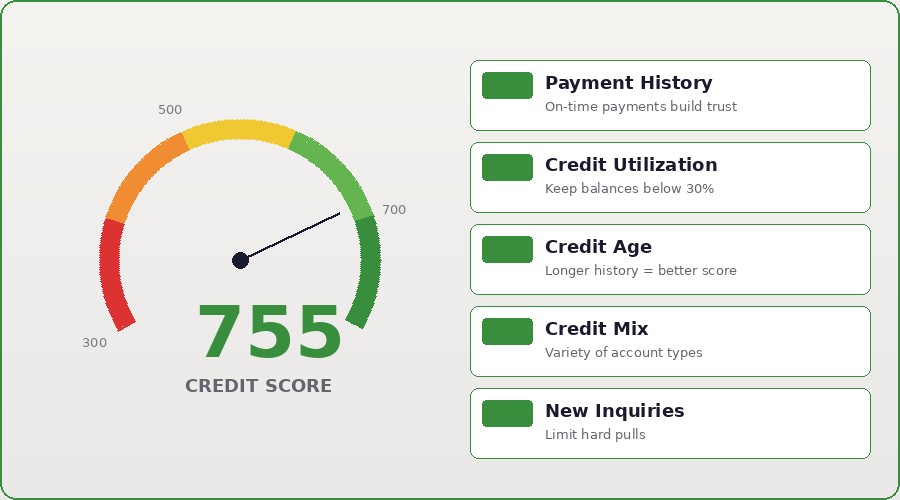

About 1 in 5 credit reports contain errors according to FTC studies — that's 40+ million Americans with wrong information on their credit reports. Errors range from incorrect balances to accounts that aren't yours to closed accounts listed as open. Your credit score is only as accurate as the information on your report, so checking it annually is non-negotiable.

Get free credit reports yearly from AnnualCreditReport.com (the only government-authorized free source). Check all three bureaus separately — Equifax, Experian, and TransUnion — because information varies. Look for incorrect accounts, wrong balances, inaccurate payment history, and accounts listed twice. Take detailed notes on any errors you find.

Once you spot an error, file a dispute in writing within 30 days of receiving your report. Send copies of documentation proving the error (account statements, payment receipts, proof of paid-off accounts). The bureau has 30 days to investigate and respond. Most bureaus process disputes faster now (10-15 days), but they're legally allowed 30 days.

Equifax, Experian, and TransUnion sometimes have different information because not all creditors report to all three bureaus. Your credit score with Equifax might be 680, with Experian 710, with TransUnion 695. This is why checking all three annually is important. If one bureau has an error the others don't, fix that bureau specifically.

Step 2: Tackle the Biggest Problems First

The IRS filed over 500,000 tax liens in recent years, but most are resolved within a few years through payment or settlement. A tax lien was historically catastrophic for credit scores, but removal from credit reports in 2018 changed the game. Now the battle is with the IRS itself, not the credit bureaus.

The best path forward depends on your tax debt size and income. Can you pay it in 30 days or less? Pay in full and the lien is released automatically within 30 days. Can't pay that fast? Apply for an installment agreement — the IRS allows monthly payments spread over 6 years or longer for amounts under $50,000. Staying current on the plan is key to avoiding levy action.

The IRS can levy (seize) wages, bank accounts, and property to collect unpaid taxes. A wage levy is brutal — the IRS can take a percentage of your paycheck without permission. You can request 'Currently Not Collectible' status if you're in extreme hardship, which stops collection action temporarily. This doesn't forgive the debt, but it freezes collection while you're struggling.

Resolving tax debt early prevents the cascade of problems: liens, levies, property seizures, and penalties that compound the original debt. Someone who owes $20,000 and ignores it could owe $35,000+ within a few years from penalties and interest. Contact the IRS or a tax professional immediately to set up a payment plan. The IRS actually prefers payment arrangements to liens and levies.

Step 3: Build Positive Credit Habits

Start your DIY credit repair by checking your reports for accuracy. Getting your free annual report is step zero. Pulling your Equifax, Experian, and TransUnion reports separately (they're usually different) gives you the full picture of what's damaging your score. Review line by line: account names, balances, payment status, account ages.

Certified mail is non-negotiable for disputes. Regular mail gets lost; certified mail with return receipt creates proof you contacted the bureau with a dispute request. The return receipt shows they received it; the certified tracking shows the date. This documentation protects you if the bureau claims they never got your dispute.

Dispute inaccurate information aggressively. If a debt is listed as 'still owed' when you paid it off, dispute it. If a late payment shows from 2019 but you were never late in 2019, dispute it. The burden is on the creditor to prove accuracy, not on you to prove inaccuracy. Many errors get removed simply because creditors can't verify the accuracy.

If DIY disputes fail after 3-4 attempts, consider hiring a credit professional. The FTC and state law give you some protection: legitimate credit repair companies charge reasonable fees, deliver realistic results, and don't claim they can remove accurate negative information. Scams promise removal of accurate information or charge upfront before delivering results — avoid those entirely.

Step 4: Consider Professional Credit Counseling

Start your DIY credit repair by checking your reports for accuracy. Getting your free annual report is step zero. Pulling your Equifax, Experian, and TransUnion reports separately (they're usually different) gives you the full picture of what's damaging your score. Review line by line: account names, balances, payment status, account ages.

Certified mail is non-negotiable for disputes. Regular mail gets lost; certified mail with return receipt creates proof you contacted the bureau with a dispute request. The return receipt shows they received it; the certified tracking shows the date. This documentation protects you if the bureau claims they never got your dispute.

Dispute inaccurate information aggressively. If a debt is listed as 'still owed' when you paid it off, dispute it. If a late payment shows from 2019 but you were never late in 2019, dispute it. The burden is on the creditor to prove accuracy, not on you to prove inaccuracy. Many errors get removed simply because creditors can't verify the accuracy.

If DIY disputes fail after 3-4 attempts, consider hiring a credit professional. The FTC and state law give you some protection: legitimate credit repair companies charge reasonable fees, deliver realistic results, and don't claim they can remove accurate negative information. Scams promise removal of accurate information or charge upfront before delivering results — avoid those entirely.