Don't Panic: Repossession Isn't the End

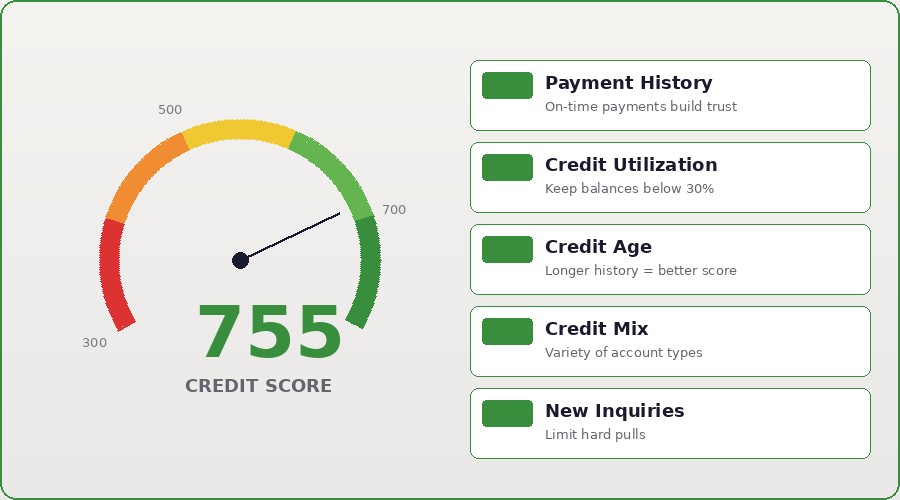

Good credit repair isn't a single move — it's a comprehensive approach combining multiple strategies simultaneously. Check your reports for errors (dispute inaccuracies), reduce balances (payment history and utilization), become an authorized user on positive accounts (mix and age), stay current on all new payments (the most important factor), and wait for negative items to age (time heals credit wounds).

The timeline for visible results is 3-6 months if you're aggressive. If you dispute errors, you might see those removed in 30-90 days. If you pay down balances, your score improves within 1-2 billing cycles. If you get added as an authorized user, that score boost happens instantly. The compounding effect of multiple moves gives you 50-100 point improvements relatively quickly.

Realistic expectations: you can't remove accurate negative information, but you can dispute inaccurate items. You can't make old items disappear (but their impact fades over time). You can build a positive credit file starting today. Recovery from 450 credit to 700 credit typically takes 18-36 months with consistent action. It's not overnight, but it's absolutely achievable.

Work with credit professionals if DIY isn't moving the needle. Good credit repair companies combine dispute expertise, creditor negotiation skills, and strategic guidance. Legitimate companies charge ongoing fees (not upfront), give honest timelines, and focus on disputing inaccuracies and negotiating with creditors. The cost is worth it if it saves you months of effort and adds years to your credit recovery timeline.

Before the Repo: Can You Stop It?

Good credit repair isn't a single move — it's a comprehensive approach combining multiple strategies simultaneously. Check your reports for errors (dispute inaccuracies), reduce balances (payment history and utilization), become an authorized user on positive accounts (mix and age), stay current on all new payments (the most important factor), and wait for negative items to age (time heals credit wounds).

The timeline for visible results is 3-6 months if you're aggressive. If you dispute errors, you might see those removed in 30-90 days. If you pay down balances, your score improves within 1-2 billing cycles. If you get added as an authorized user, that score boost happens instantly. The compounding effect of multiple moves gives you 50-100 point improvements relatively quickly.

Realistic expectations: you can't remove accurate negative information, but you can dispute inaccurate items. You can't make old items disappear (but their impact fades over time). You can build a positive credit file starting today. Recovery from 450 credit to 700 credit typically takes 18-36 months with consistent action. It's not overnight, but it's absolutely achievable.

Work with credit professionals if DIY isn't moving the needle. Good credit repair companies combine dispute expertise, creditor negotiation skills, and strategic guidance. Legitimate companies charge ongoing fees (not upfront), give honest timelines, and focus on disputing inaccuracies and negotiating with creditors. The cost is worth it if it saves you months of effort and adds years to your credit recovery timeline.

Dealing with the Deficiency Balance

Good credit repair isn't a single move — it's a comprehensive approach combining multiple strategies simultaneously. Check your reports for errors (dispute inaccuracies), reduce balances (payment history and utilization), become an authorized user on positive accounts (mix and age), stay current on all new payments (the most important factor), and wait for negative items to age (time heals credit wounds).

The timeline for visible results is 3-6 months if you're aggressive. If you dispute errors, you might see those removed in 30-90 days. If you pay down balances, your score improves within 1-2 billing cycles. If you get added as an authorized user, that score boost happens instantly. The compounding effect of multiple moves gives you 50-100 point improvements relatively quickly.

Realistic expectations: you can't remove accurate negative information, but you can dispute inaccurate items. You can't make old items disappear (but their impact fades over time). You can build a positive credit file starting today. Recovery from 450 credit to 700 credit typically takes 18-36 months with consistent action. It's not overnight, but it's absolutely achievable.

Work with credit professionals if DIY isn't moving the needle. Good credit repair companies combine dispute expertise, creditor negotiation skills, and strategic guidance. Legitimate companies charge ongoing fees (not upfront), give honest timelines, and focus on disputing inaccuracies and negotiating with creditors. The cost is worth it if it saves you months of effort and adds years to your credit recovery timeline.

How to Get Back on the Road

Start your DIY credit repair by checking your reports for accuracy. Getting your free annual report is step zero. Pulling your Equifax, Experian, and TransUnion reports separately (they're usually different) gives you the full picture of what's damaging your score. Review line by line: account names, balances, payment status, account ages.

Certified mail is non-negotiable for disputes. Regular mail gets lost; certified mail with return receipt creates proof you contacted the bureau with a dispute request. The return receipt shows they received it; the certified tracking shows the date. This documentation protects you if the bureau claims they never got your dispute.

Dispute inaccurate information aggressively. If a debt is listed as 'still owed' when you paid it off, dispute it. If a late payment shows from 2019 but you were never late in 2019, dispute it. The burden is on the creditor to prove accuracy, not on you to prove inaccuracy. Many errors get removed simply because creditors can't verify the accuracy.

If DIY disputes fail after 3-4 attempts, consider hiring a credit professional. The FTC and state law give you some protection: legitimate credit repair companies charge reasonable fees, deliver realistic results, and don't claim they can remove accurate negative information. Scams promise removal of accurate information or charge upfront before delivering results — avoid those entirely.

Credit Recovery with 755CreditScore

Good credit repair isn't a single move — it's a comprehensive approach combining multiple strategies simultaneously. Check your reports for errors (dispute inaccuracies), reduce balances (payment history and utilization), become an authorized user on positive accounts (mix and age), stay current on all new payments (the most important factor), and wait for negative items to age (time heals credit wounds).

The timeline for visible results is 3-6 months if you're aggressive. If you dispute errors, you might see those removed in 30-90 days. If you pay down balances, your score improves within 1-2 billing cycles. If you get added as an authorized user, that score boost happens instantly. The compounding effect of multiple moves gives you 50-100 point improvements relatively quickly.

Realistic expectations: you can't remove accurate negative information, but you can dispute inaccurate items. You can't make old items disappear (but their impact fades over time). You can build a positive credit file starting today. Recovery from 450 credit to 700 credit typically takes 18-36 months with consistent action. It's not overnight, but it's absolutely achievable.

Work with credit professionals if DIY isn't moving the needle. Good credit repair companies combine dispute expertise, creditor negotiation skills, and strategic guidance. Legitimate companies charge ongoing fees (not upfront), give honest timelines, and focus on disputing inaccuracies and negotiating with creditors. The cost is worth it if it saves you months of effort and adds years to your credit recovery timeline.