Bankruptcy Basics: Chapter 7 vs Chapter 13

Bankruptcy isn't the end of the world, though it feels like it when you file. Chapter 7 wipes out most unsecured debts — credit cards, medical bills, personal loans — but you lose assets. Chapter 13 restructures your debt into a 3-5 year repayment plan while you keep your property. Texas has powerful homestead protections: you can keep your primary residence even in Chapter 7, up to a certain value. That's a huge advantage over many states.

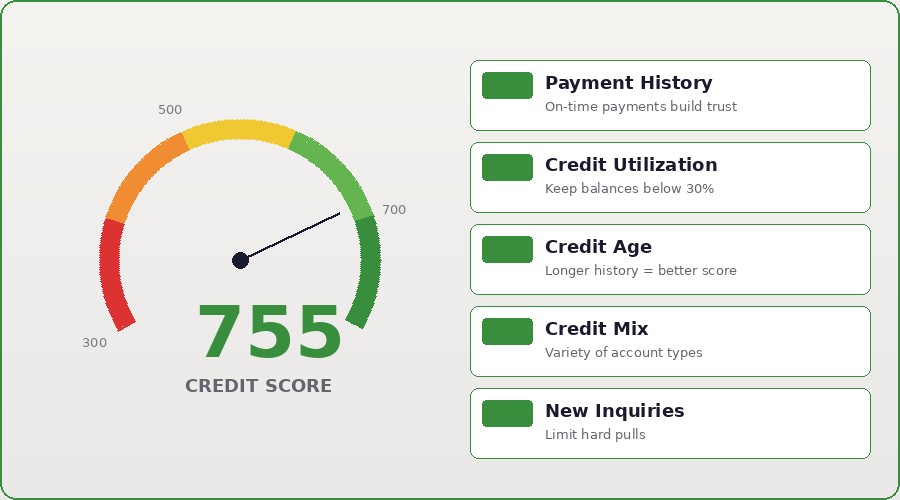

A bankruptcy stays on your credit report for 7 years (Chapter 13) to 10 years (Chapter 7). That sounds devastating, but here's what most people don't realize: you can rebuild your credit during those 7-10 years. People often get back to 700+ scores within 2-3 years after discharge if they use secured cards, become an authorized user on positive accounts, and keep all new payments current.

The means test determines whether you qualify for Chapter 7 or must file Chapter 13. Texas courts look at your income versus the state median to decide if you have 'disposable income' available for a repayment plan. Many Texans qualify for Chapter 7 straight-up, erasing debts without repayment. The Houston/Harris County area has many experienced bankruptcy trustees who understand these rules.

Rebuilding after bankruptcy starts the day your discharge is granted. Get a secured credit card with a small deposit ($500-$1000), use it for small purchases, and pay it in full monthly. After 6-12 months of perfect payments, you can apply for a standard card. The bankruptcy entry fades in power over time — after 3 years with perfect new credit history, it's almost a non-factor for many lenders.

How Bankruptcy Affects Your Credit Score

Bankruptcy isn't the end of the world, though it feels like it when you file. Chapter 7 wipes out most unsecured debts — credit cards, medical bills, personal loans — but you lose assets. Chapter 13 restructures your debt into a 3-5 year repayment plan while you keep your property. Texas has powerful homestead protections: you can keep your primary residence even in Chapter 7, up to a certain value. That's a huge advantage over many states.

A bankruptcy stays on your credit report for 7 years (Chapter 13) to 10 years (Chapter 7). That sounds devastating, but here's what most people don't realize: you can rebuild your credit during those 7-10 years. People often get back to 700+ scores within 2-3 years after discharge if they use secured cards, become an authorized user on positive accounts, and keep all new payments current.

The means test determines whether you qualify for Chapter 7 or must file Chapter 13. Texas courts look at your income versus the state median to decide if you have 'disposable income' available for a repayment plan. Many Texans qualify for Chapter 7 straight-up, erasing debts without repayment. The Houston/Harris County area has many experienced bankruptcy trustees who understand these rules.

Rebuilding after bankruptcy starts the day your discharge is granted. Get a secured credit card with a small deposit ($500-$1000), use it for small purchases, and pay it in full monthly. After 6-12 months of perfect payments, you can apply for a standard card. The bankruptcy entry fades in power over time — after 3 years with perfect new credit history, it's almost a non-factor for many lenders.

Life After Bankruptcy in Texas

Chapter 7 bankruptcy liquidates assets to pay creditors, then discharges remaining debt. Chapter 13 keeps your assets but requires you to repay debts on a 3-5 year plan. The choice depends on your income and assets. If you have a house, car, and stable income, Chapter 13 might be better. If you're underwater and have no assets, Chapter 7 clears the deck.

Texas homestead laws are exceptionally debtor-friendly. Your primary residence is protected in bankruptcy up to a certain value (currently around $420k in most of Texas). This means you could have a $300k house, owe $200k in credit card debt, and keep the house by filing Chapter 13. Many states don't offer anywhere near this protection.

The emotional trauma of bankruptcy is real, but the legal recovery is faster than you'd think. After Chapter 7 discharge, you can get credit offers within weeks. After Chapter 13 discharge, you're no longer in active repayment and lenders see you as lower-risk. Combined with secured cards and becoming an authorized user on positive accounts, you can realistically target a 650+ score within 18 months post-discharge.

Filing costs $400-$500 in court fees plus attorney fees ($1000-$3000 depending on complexity). Many bankruptcy attorneys offer payment plans since they understand you don't have liquid money. The cost is painful but far cheaper than drowning in debt for years. Consult with at least 2 attorneys to compare approaches and see who you trust with the process.

Rebuilding Your Credit After Bankruptcy

Chapter 7 bankruptcy liquidates assets to pay creditors, then discharges remaining debt. Chapter 13 keeps your assets but requires you to repay debts on a 3-5 year plan. The choice depends on your income and assets. If you have a house, car, and stable income, Chapter 13 might be better. If you're underwater and have no assets, Chapter 7 clears the deck.

Texas homestead laws are exceptionally debtor-friendly. Your primary residence is protected in bankruptcy up to a certain value (currently around $420k in most of Texas). This means you could have a $300k house, owe $200k in credit card debt, and keep the house by filing Chapter 13. Many states don't offer anywhere near this protection.

The emotional trauma of bankruptcy is real, but the legal recovery is faster than you'd think. After Chapter 7 discharge, you can get credit offers within weeks. After Chapter 13 discharge, you're no longer in active repayment and lenders see you as lower-risk. Combined with secured cards and becoming an authorized user on positive accounts, you can realistically target a 650+ score within 18 months post-discharge.

Filing costs $400-$500 in court fees plus attorney fees ($1000-$3000 depending on complexity). Many bankruptcy attorneys offer payment plans since they understand you don't have liquid money. The cost is painful but far cheaper than drowning in debt for years. Consult with at least 2 attorneys to compare approaches and see who you trust with the process.

755CreditScore Can Help You Rebuild

Credit repair is fundamentally about managing three factors: accuracy of reports, payment behavior going forward, and aging of negative items. You can't change history, but you can correct inaccuracies, prove you're financially responsible now, and let time fade old damage. Most people dramatically underestimate what's possible because they think accurate negative information is permanent (it fades in power over time).

Start by checking your reports (free at AnnualCreditReport.com), identifying errors, and disputing inaccuracies in writing. While disputes process, focus on new credit behavior: pay every bill on time, reduce existing balances, avoid new hard inquiries. This dual approach of fixing reports while building positive history compounds over months.

Add yourself to positive accounts as an authorized user if possible. Family or friends with excellent credit and high limits can add you to their account. Their payment history and age show up on your report, boosting your score instantly by 50-100 points in many cases. There are no downsides if the primary account holder has perfect payment history and low utilization.

Becoming current on all accounts is critical. Stop the bleeding first. If you have delinquent accounts, get current immediately. One month of current payments doesn't erase the delinquency history, but it stops the daily credit score damage. After 3-6 months of current payments on previously delinquent accounts, you'll see significant score improvements.