What Is a Civil Judgment?

A judgment is a court order declaring you legally owe a debt and giving the creditor the right to collect it — sometimes by garnishing your wages. Many judgments are 'default judgments,' meaning you didn't show up to court and lost by default. Texas wage garnishment allows creditors to take up to 25% of your wages, and the judgment stays on your report for 7 years.

Default judgments are the most common and the easiest to prevent — you just have to show up to court or respond to the lawsuit. If you've been sued and received papers, respond immediately, even if it's just to ask for more time. Ignoring a lawsuit is how you end up with a $5,000 judgment turning into $8,000 through court costs and attorney fees.

You have options to fight a judgment after it's entered. You can file a 'motion to vacate' if you weren't properly served, didn't know about the hearing, or had a legitimate reason for missing court. Texas law allows vacating a judgment if you file within a reasonable time and have a valid excuse. The standard is strict, but it's worth trying if you weren't properly notified.

Paying off a judgment doesn't automatically remove it from your credit report. You need a 'satisfaction of judgment' filed by the creditor confirming it's paid. Get this in writing when you settle. The paid judgment still appears on your report but shows 'satisfied,' which looks better than an unsatisfied judgment and has less score impact.

How Judgments Affect Your Financial Life

A judgment is a court order declaring you legally owe a debt and giving the creditor the right to collect it — sometimes by garnishing your wages. Many judgments are 'default judgments,' meaning you didn't show up to court and lost by default. Texas wage garnishment allows creditors to take up to 25% of your wages, and the judgment stays on your report for 7 years.

Default judgments are the most common and the easiest to prevent — you just have to show up to court or respond to the lawsuit. If you've been sued and received papers, respond immediately, even if it's just to ask for more time. Ignoring a lawsuit is how you end up with a $5,000 judgment turning into $8,000 through court costs and attorney fees.

You have options to fight a judgment after it's entered. You can file a 'motion to vacate' if you weren't properly served, didn't know about the hearing, or had a legitimate reason for missing court. Texas law allows vacating a judgment if you file within a reasonable time and have a valid excuse. The standard is strict, but it's worth trying if you weren't properly notified.

Paying off a judgment doesn't automatically remove it from your credit report. You need a 'satisfaction of judgment' filed by the creditor confirming it's paid. Get this in writing when you settle. The paid judgment still appears on your report but shows 'satisfied,' which looks better than an unsatisfied judgment and has less score impact.

Judgment vs Satisfied Judgment

Getting sued by a creditor is serious, but the court process gives you opportunities to fight. Creditors must properly serve you with papers — if they don't, you can get the case dismissed. Many creditors use sloppy service practices, and courts sometimes throw out cases for improper notice. Don't ignore the papers hoping it goes away; engage the system.

If a judgment already exists against you, explore a 'vacation of judgment' motion. This is harder after time passes, but it's possible if you can show you weren't properly served, didn't know about the hearing, or had a legitimate emergency that prevented your appearance. You'll need an affidavit explaining your situation and possibly attorney help, but it's worth fighting if you have a valid excuse.

Texas has specific wage garnishment limits: creditors can take up to 25% of your weekly disposable income, but never more than 30 times the minimum wage per week. If you're already struggling financially, you can claim hardship and potentially reduce or stop the garnishment. The court will consider your expenses versus income.

A judgment's impact on your credit fades over time, but it stays for 7 years from entry. Even if you can't immediately pay or vacate it, keeping current on new accounts and building positive credit history gradually reduces its impact. After 3 years of perfect new credit, lenders are more willing to look past an older judgment. After 7 years, it's gone from your report entirely.

Options for Resolving Judgments in Texas

Getting sued by a creditor is serious, but the court process gives you opportunities to fight. Creditors must properly serve you with papers — if they don't, you can get the case dismissed. Many creditors use sloppy service practices, and courts sometimes throw out cases for improper notice. Don't ignore the papers hoping it goes away; engage the system.

If a judgment already exists against you, explore a 'vacation of judgment' motion. This is harder after time passes, but it's possible if you can show you weren't properly served, didn't know about the hearing, or had a legitimate emergency that prevented your appearance. You'll need an affidavit explaining your situation and possibly attorney help, but it's worth fighting if you have a valid excuse.

Texas has specific wage garnishment limits: creditors can take up to 25% of your weekly disposable income, but never more than 30 times the minimum wage per week. If you're already struggling financially, you can claim hardship and potentially reduce or stop the garnishment. The court will consider your expenses versus income.

A judgment's impact on your credit fades over time, but it stays for 7 years from entry. Even if you can't immediately pay or vacate it, keeping current on new accounts and building positive credit history gradually reduces its impact. After 3 years of perfect new credit, lenders are more willing to look past an older judgment. After 7 years, it's gone from your report entirely.

Professional Help from 755CreditScore

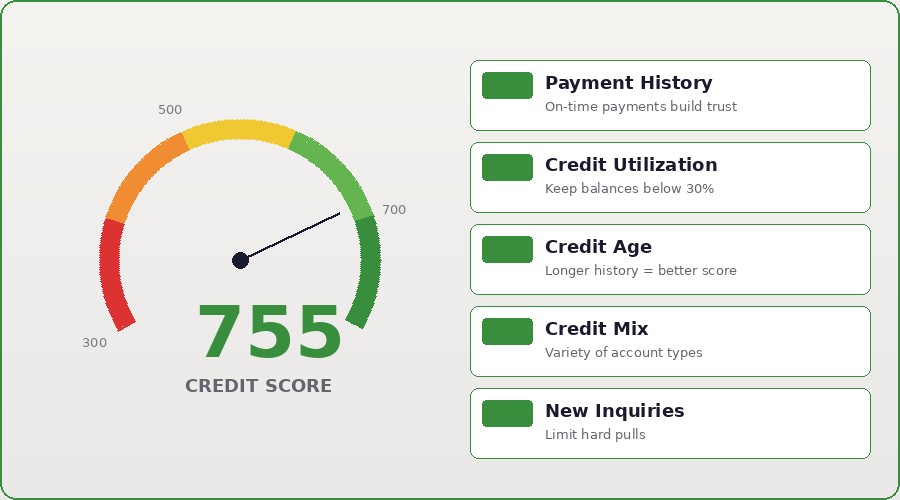

Credit repair is fundamentally about managing three factors: accuracy of reports, payment behavior going forward, and aging of negative items. You can't change history, but you can correct inaccuracies, prove you're financially responsible now, and let time fade old damage. Most people dramatically underestimate what's possible because they think accurate negative information is permanent (it fades in power over time).

Start by checking your reports (free at AnnualCreditReport.com), identifying errors, and disputing inaccuracies in writing. While disputes process, focus on new credit behavior: pay every bill on time, reduce existing balances, avoid new hard inquiries. This dual approach of fixing reports while building positive history compounds over months.

Add yourself to positive accounts as an authorized user if possible. Family or friends with excellent credit and high limits can add you to their account. Their payment history and age show up on your report, boosting your score instantly by 50-100 points in many cases. There are no downsides if the primary account holder has perfect payment history and low utilization.

Becoming current on all accounts is critical. Stop the bleeding first. If you have delinquent accounts, get current immediately. One month of current payments doesn't erase the delinquency history, but it stops the daily credit score damage. After 3-6 months of current payments on previously delinquent accounts, you'll see significant score improvements.