What Are Collections and How Do They Get on Your Report?

Collections happen to more people than you'd think. Maybe a medical bill got lost, or a credit card company stopped trying to reach you. When debts go unpaid for 120-180 days, creditors usually give up and sell your account to a collection agency.

That's when things get scary for your credit score. A collection account can drop your score by 50-100 points or more — sometimes instantly. And it doesn't matter if the debt is small; even a $200 collection can devastate an otherwise decent credit profile.

The worst part? Collections stay on your report for seven years. But here's the thing — you have options. You can dispute them, negotiate with the agency, or work with a professional to get them removed. It's not hopeless.

How Collections Damage Your Credit Score

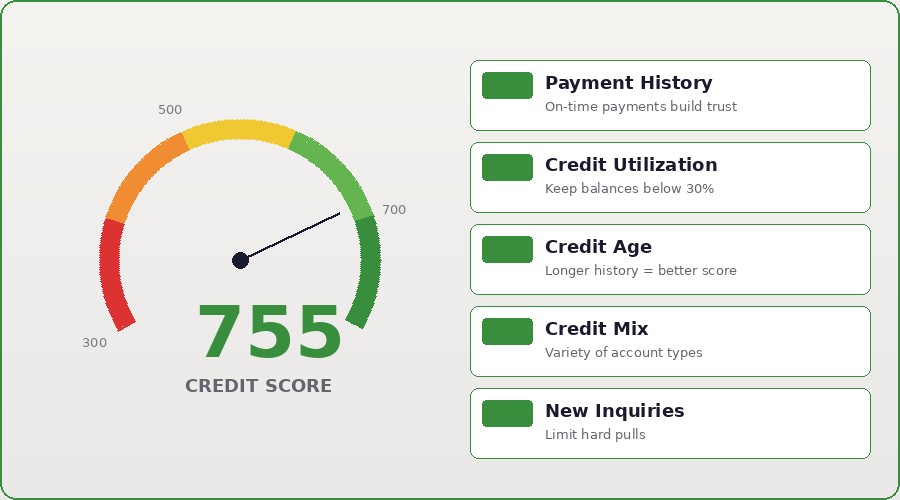

Think of your credit score like a complex math equation. Payment history is the biggest piece — it's worth 35% of your FICO score. Collections hit you twice: once as a late payment, and again as a collection account on your report.

Even a small collection — say $150 — can hurt your score significantly. Lenders see collections and think 'this person doesn't pay their debts.' That perception costs you. You'll face higher interest rates, stricter lending terms, or outright rejections.

Here's what surprises most people: a paid collection still hurts your score, though not quite as much. The damage is done when it's reported, not when you pay it off. That's why you shouldn't just pay a collection without a strategy.

Your Rights When Dealing with Collectors

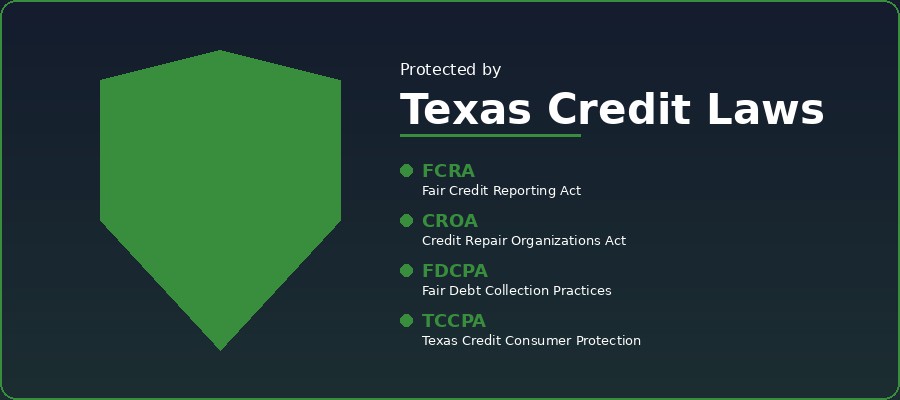

The Fair Debt Collection Practices Act (FDCPA) is your shield against aggressive collectors. They can't call before 8am or after 9pm. They can't harass you, use profanity, or threaten you with jail time. They can't contact your boss or friends.

You have the right to dispute any collection. Send a validation letter (certified mail) asking them to prove the debt is yours. They have 30 days to respond. If they can't validate it, they're supposed to remove it from your report.

You can also write to the credit bureaus and tell them the collection is wrong. If the collection agency can't verify the info, the bureau must remove it. Don't assume you have to pay — always question the validity first.

At 755CreditScore, we help clients navigate these challenges and rebuild their credit.

Steps to Remove Collections from Your Report

Start by getting a copy of your credit report from all three bureaus. Look for the collection account and make sure it's accurate. If it's wrong — if the amount is off, or if it's not even your debt — you have grounds to dispute it.

Send a validation letter to the collection agency (not the credit bureau) via certified mail. Ask them to provide proof that you owe this debt. Many collections are so old that agencies can't find documentation. If they can't validate within 30 days, the FDCPA requires them to stop collection efforts.

If they do validate it, you can negotiate. Some agencies will accept a 'pay-for-delete' agreement — they remove the collection if you pay. Get everything in writing. You can also dispute directly with the bureaus if you find errors, or ask for a goodwill removal from the original creditor.

Why Professional Help Makes a Difference

Collections disputes can get complicated. You need to know what evidence matters, how to word your letters, and when to push back. Professionals know the ins and outs of the dispute process and have established relationships with the bureaus.

A professional credit counselor can look at your entire credit profile and prioritize which collections to tackle first. Some debts are worth fighting harder than others. Sometimes paying one strategically is better than disputing another.

Many clients find that professional help speeds up the process. What might take you six months of learning and trying might take a professional three months. Plus, if a bureau denies your dispute, we know how to escalate to the CFPB and keep pushing.

At 755CreditScore, we help clients navigate these challenges and rebuild their credit.