Why Houston Residents Need Good Credit

Houston's booming oil and gas industry means employment volatility that whacks credit scores when layoffs hit. 2015 had massive energy downturn layoffs that decimated Houston credit scores. Gas station workers, office staff, engineers — everyone affected took credit hits when they missed payments during the transition. If this sounds like you, you're not alone in Houston, and recovery is possible.

Cost of living in Houston is reasonable compared to coastal cities, but that's relative. Mortgage debt, property taxes, and insurance still strain plenty of Houston families. Bad credit means higher interest rates on mortgages — that 0.5% rate difference on a $300,000 mortgage costs $50,000+ over the life of the loan. Better credit in Houston can mean serious money in your pocket.

The Houston-area suburbs (Pearland, Sugar Land, Katy) are growing fast with young families stretching finances. Mortgage pre-approval requires good credit; building credit strategically before house hunting saves money and gets you approved for better rates. We work with hundreds of Houston families annually fixing credit before major purchases.

If you're in Greater Houston and struggling with credit, the system is fixable. Local economy factors don't matter as much as consistent action. Get current, dispute errors, build positive history, and call 832-696-0755 for a free consultation on your specific situation.

DIY Credit Repair: The Basics

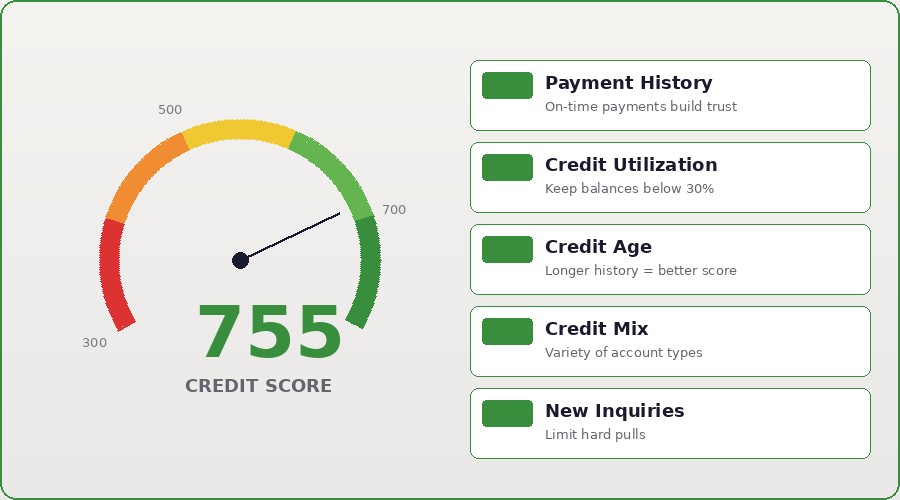

Start your DIY credit repair by checking your reports for accuracy. Getting your free annual report is step zero. Pulling your Equifax, Experian, and TransUnion reports separately (they're usually different) gives you the full picture of what's damaging your score. Review line by line: account names, balances, payment status, account ages.

Certified mail is non-negotiable for disputes. Regular mail gets lost; certified mail with return receipt creates proof you contacted the bureau with a dispute request. The return receipt shows they received it; the certified tracking shows the date. This documentation protects you if the bureau claims they never got your dispute.

Dispute inaccurate information aggressively. If a debt is listed as 'still owed' when you paid it off, dispute it. If a late payment shows from 2019 but you were never late in 2019, dispute it. The burden is on the creditor to prove accuracy, not on you to prove inaccuracy. Many errors get removed simply because creditors can't verify the accuracy.

If DIY disputes fail after 3-4 attempts, consider hiring a credit professional. The FTC and state law give you some protection: legitimate credit repair companies charge reasonable fees, deliver realistic results, and don't claim they can remove accurate negative information. Scams promise removal of accurate information or charge upfront before delivering results — avoid those entirely.

Houston-Specific Resources

Houston's booming oil and gas industry means employment volatility that whacks credit scores when layoffs hit. 2015 had massive energy downturn layoffs that decimated Houston credit scores. Gas station workers, office staff, engineers — everyone affected took credit hits when they missed payments during the transition. If this sounds like you, you're not alone in Houston, and recovery is possible.

Cost of living in Houston is reasonable compared to coastal cities, but that's relative. Mortgage debt, property taxes, and insurance still strain plenty of Houston families. Bad credit means higher interest rates on mortgages — that 0.5% rate difference on a $300,000 mortgage costs $50,000+ over the life of the loan. Better credit in Houston can mean serious money in your pocket.

The Houston-area suburbs (Pearland, Sugar Land, Katy) are growing fast with young families stretching finances. Mortgage pre-approval requires good credit; building credit strategically before house hunting saves money and gets you approved for better rates. We work with hundreds of Houston families annually fixing credit before major purchases.

If you're in Greater Houston and struggling with credit, the system is fixable. Local economy factors don't matter as much as consistent action. Get current, dispute errors, build positive history, and call 832-696-0755 for a free consultation on your specific situation.

Common DIY Mistakes to Avoid

Start your DIY credit repair by checking your reports for accuracy. Getting your free annual report is step zero. Pulling your Equifax, Experian, and TransUnion reports separately (they're usually different) gives you the full picture of what's damaging your score. Review line by line: account names, balances, payment status, account ages.

Certified mail is non-negotiable for disputes. Regular mail gets lost; certified mail with return receipt creates proof you contacted the bureau with a dispute request. The return receipt shows they received it; the certified tracking shows the date. This documentation protects you if the bureau claims they never got your dispute.

Dispute inaccurate information aggressively. If a debt is listed as 'still owed' when you paid it off, dispute it. If a late payment shows from 2019 but you were never late in 2019, dispute it. The burden is on the creditor to prove accuracy, not on you to prove inaccuracy. Many errors get removed simply because creditors can't verify the accuracy.

If DIY disputes fail after 3-4 attempts, consider hiring a credit professional. The FTC and state law give you some protection: legitimate credit repair companies charge reasonable fees, deliver realistic results, and don't claim they can remove accurate negative information. Scams promise removal of accurate information or charge upfront before delivering results — avoid those entirely.

When to Hire Professional Help

Credit repair is fundamentally about managing three factors: accuracy of reports, payment behavior going forward, and aging of negative items. You can't change history, but you can correct inaccuracies, prove you're financially responsible now, and let time fade old damage. Most people dramatically underestimate what's possible because they think accurate negative information is permanent (it fades in power over time).

Start by checking your reports (free at AnnualCreditReport.com), identifying errors, and disputing inaccuracies in writing. While disputes process, focus on new credit behavior: pay every bill on time, reduce existing balances, avoid new hard inquiries. This dual approach of fixing reports while building positive history compounds over months.

Add yourself to positive accounts as an authorized user if possible. Family or friends with excellent credit and high limits can add you to their account. Their payment history and age show up on your report, boosting your score instantly by 50-100 points in many cases. There are no downsides if the primary account holder has perfect payment history and low utilization.

Becoming current on all accounts is critical. Stop the bleeding first. If you have delinquent accounts, get current immediately. One month of current payments doesn't erase the delinquency history, but it stops the daily credit score damage. After 3-6 months of current payments on previously delinquent accounts, you'll see significant score improvements.