The Stress of Living with Bad Credit

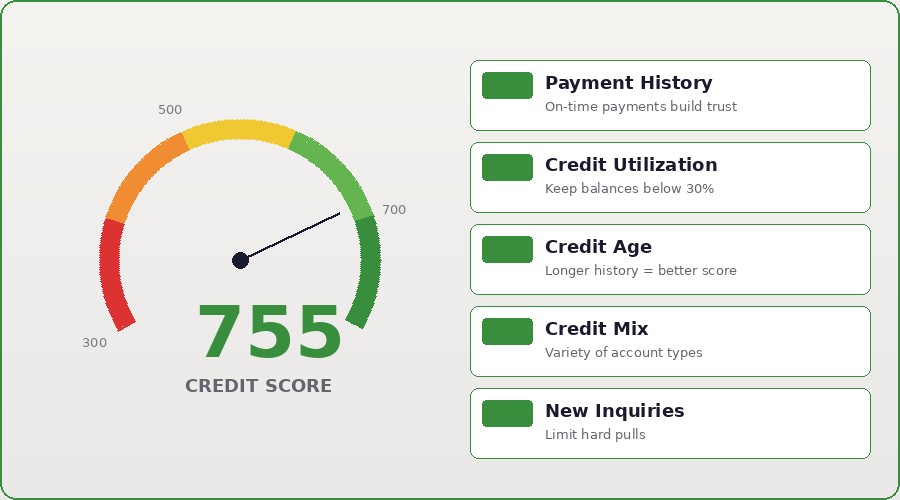

Credit repair is fundamentally about managing three factors: accuracy of reports, payment behavior going forward, and aging of negative items. You can't change history, but you can correct inaccuracies, prove you're financially responsible now, and let time fade old damage. Most people dramatically underestimate what's possible because they think accurate negative information is permanent (it fades in power over time).

Start by checking your reports (free at AnnualCreditReport.com), identifying errors, and disputing inaccuracies in writing. While disputes process, focus on new credit behavior: pay every bill on time, reduce existing balances, avoid new hard inquiries. This dual approach of fixing reports while building positive history compounds over months.

Add yourself to positive accounts as an authorized user if possible. Family or friends with excellent credit and high limits can add you to their account. Their payment history and age show up on your report, boosting your score instantly by 50-100 points in many cases. There are no downsides if the primary account holder has perfect payment history and low utilization.

Becoming current on all accounts is critical. Stop the bleeding first. If you have delinquent accounts, get current immediately. One month of current payments doesn't erase the delinquency history, but it stops the daily credit score damage. After 3-6 months of current payments on previously delinquent accounts, you'll see significant score improvements.

Taking the First Step Toward Peace of Mind

The IRS filed over 500,000 tax liens in recent years, but most are resolved within a few years through payment or settlement. A tax lien was historically catastrophic for credit scores, but removal from credit reports in 2018 changed the game. Now the battle is with the IRS itself, not the credit bureaus.

The best path forward depends on your tax debt size and income. Can you pay it in 30 days or less? Pay in full and the lien is released automatically within 30 days. Can't pay that fast? Apply for an installment agreement — the IRS allows monthly payments spread over 6 years or longer for amounts under $50,000. Staying current on the plan is key to avoiding levy action.

The IRS can levy (seize) wages, bank accounts, and property to collect unpaid taxes. A wage levy is brutal — the IRS can take a percentage of your paycheck without permission. You can request 'Currently Not Collectible' status if you're in extreme hardship, which stops collection action temporarily. This doesn't forgive the debt, but it freezes collection while you're struggling.

Resolving tax debt early prevents the cascade of problems: liens, levies, property seizures, and penalties that compound the original debt. Someone who owes $20,000 and ignores it could owe $35,000+ within a few years from penalties and interest. Contact the IRS or a tax professional immediately to set up a payment plan. The IRS actually prefers payment arrangements to liens and levies.

Watching Your Score Improve Changes Everything

Credit repair is fundamentally about managing three factors: accuracy of reports, payment behavior going forward, and aging of negative items. You can't change history, but you can correct inaccuracies, prove you're financially responsible now, and let time fade old damage. Most people dramatically underestimate what's possible because they think accurate negative information is permanent (it fades in power over time).

Start by checking your reports (free at AnnualCreditReport.com), identifying errors, and disputing inaccuracies in writing. While disputes process, focus on new credit behavior: pay every bill on time, reduce existing balances, avoid new hard inquiries. This dual approach of fixing reports while building positive history compounds over months.

Add yourself to positive accounts as an authorized user if possible. Family or friends with excellent credit and high limits can add you to their account. Their payment history and age show up on your report, boosting your score instantly by 50-100 points in many cases. There are no downsides if the primary account holder has perfect payment history and low utilization.

Becoming current on all accounts is critical. Stop the bleeding first. If you have delinquent accounts, get current immediately. One month of current payments doesn't erase the delinquency history, but it stops the daily credit score damage. After 3-6 months of current payments on previously delinquent accounts, you'll see significant score improvements.

Financial Serenity Is a Phone Call Away

Credit repair is fundamentally about managing three factors: accuracy of reports, payment behavior going forward, and aging of negative items. You can't change history, but you can correct inaccuracies, prove you're financially responsible now, and let time fade old damage. Most people dramatically underestimate what's possible because they think accurate negative information is permanent (it fades in power over time).

Start by checking your reports (free at AnnualCreditReport.com), identifying errors, and disputing inaccuracies in writing. While disputes process, focus on new credit behavior: pay every bill on time, reduce existing balances, avoid new hard inquiries. This dual approach of fixing reports while building positive history compounds over months.

Add yourself to positive accounts as an authorized user if possible. Family or friends with excellent credit and high limits can add you to their account. Their payment history and age show up on your report, boosting your score instantly by 50-100 points in many cases. There are no downsides if the primary account holder has perfect payment history and low utilization.

Becoming current on all accounts is critical. Stop the bleeding first. If you have delinquent accounts, get current immediately. One month of current payments doesn't erase the delinquency history, but it stops the daily credit score damage. After 3-6 months of current payments on previously delinquent accounts, you'll see significant score improvements.

Let 755CreditScore Lift the Weight

Credit repair is fundamentally about managing three factors: accuracy of reports, payment behavior going forward, and aging of negative items. You can't change history, but you can correct inaccuracies, prove you're financially responsible now, and let time fade old damage. Most people dramatically underestimate what's possible because they think accurate negative information is permanent (it fades in power over time).

Start by checking your reports (free at AnnualCreditReport.com), identifying errors, and disputing inaccuracies in writing. While disputes process, focus on new credit behavior: pay every bill on time, reduce existing balances, avoid new hard inquiries. This dual approach of fixing reports while building positive history compounds over months.

Add yourself to positive accounts as an authorized user if possible. Family or friends with excellent credit and high limits can add you to their account. Their payment history and age show up on your report, boosting your score instantly by 50-100 points in many cases. There are no downsides if the primary account holder has perfect payment history and low utilization.

Becoming current on all accounts is critical. Stop the bleeding first. If you have delinquent accounts, get current immediately. One month of current payments doesn't erase the delinquency history, but it stops the daily credit score damage. After 3-6 months of current payments on previously delinquent accounts, you'll see significant score improvements.