Who Are the Three Credit Bureaus?

The three major credit bureaus — Equifax, Experian, and TransUnion — maintain credit reports on almost all Americans with credit history. These reports include payment history, credit accounts, inquiries, and negative items. Lenders use these reports to decide whether to approve you and what interest rate to charge. Inaccurate information directly impacts your ability to borrow.

Dispute errors in writing, not by phone. Send certified mail with return receipt to prove you contacted the bureau. Include copies (not originals) of documentation supporting your dispute. The bureau must investigate within 30 days and report back. If they can't verify the accuracy of the error, they're required to remove it or correct it.

Some errors are creditor reporting mistakes, not bureau mistakes. If a creditor reported an account closed when it's open, or reported a late payment that didn't happen, dispute it with both the creditor and the bureau. The creditor must update their reporting within 15 days; the bureau must update within 30 days. Get both in writing.

Your credit report is free to check once yearly from AnnualCreditReport.com. Credit monitoring services cost extra ($10-15 monthly) but monitor your report automatically for changes and alert you to new accounts or inquiries. If you've had fraud or are a financial nervous person, it might be worth the cost. But the free annual report is sufficient if you check it carefully yearly.

Why Your Scores Differ Between Bureaus

About 1 in 5 credit reports contain errors according to FTC studies — that's 40+ million Americans with wrong information on their credit reports. Errors range from incorrect balances to accounts that aren't yours to closed accounts listed as open. Your credit score is only as accurate as the information on your report, so checking it annually is non-negotiable.

Get free credit reports yearly from AnnualCreditReport.com (the only government-authorized free source). Check all three bureaus separately — Equifax, Experian, and TransUnion — because information varies. Look for incorrect accounts, wrong balances, inaccurate payment history, and accounts listed twice. Take detailed notes on any errors you find.

Once you spot an error, file a dispute in writing within 30 days of receiving your report. Send copies of documentation proving the error (account statements, payment receipts, proof of paid-off accounts). The bureau has 30 days to investigate and respond. Most bureaus process disputes faster now (10-15 days), but they're legally allowed 30 days.

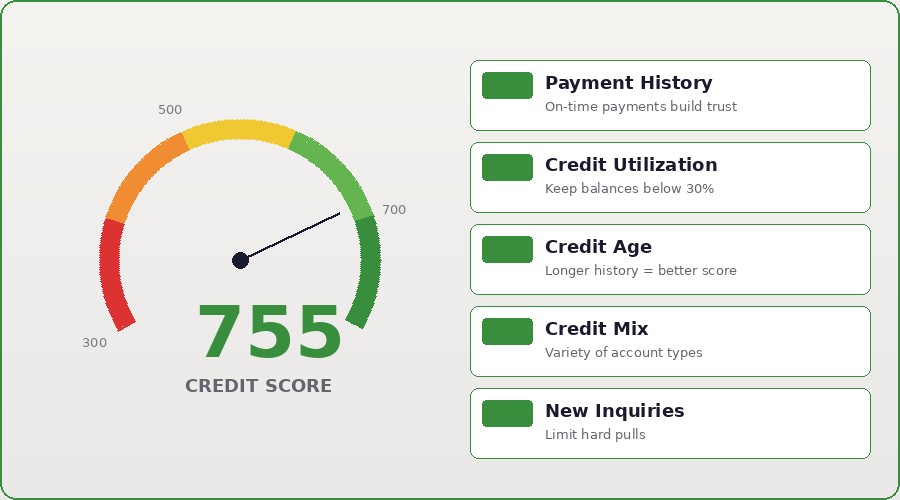

Equifax, Experian, and TransUnion sometimes have different information because not all creditors report to all three bureaus. Your credit score with Equifax might be 680, with Experian 710, with TransUnion 695. This is why checking all three annually is important. If one bureau has an error the others don't, fix that bureau specifically.

How to Get Your Free Credit Reports

About 1 in 5 credit reports contain errors according to FTC studies — that's 40+ million Americans with wrong information on their credit reports. Errors range from incorrect balances to accounts that aren't yours to closed accounts listed as open. Your credit score is only as accurate as the information on your report, so checking it annually is non-negotiable.

Get free credit reports yearly from AnnualCreditReport.com (the only government-authorized free source). Check all three bureaus separately — Equifax, Experian, and TransUnion — because information varies. Look for incorrect accounts, wrong balances, inaccurate payment history, and accounts listed twice. Take detailed notes on any errors you find.

Once you spot an error, file a dispute in writing within 30 days of receiving your report. Send copies of documentation proving the error (account statements, payment receipts, proof of paid-off accounts). The bureau has 30 days to investigate and respond. Most bureaus process disputes faster now (10-15 days), but they're legally allowed 30 days.

Equifax, Experian, and TransUnion sometimes have different information because not all creditors report to all three bureaus. Your credit score with Equifax might be 680, with Experian 710, with TransUnion 695. This is why checking all three annually is important. If one bureau has an error the others don't, fix that bureau specifically.

Disputing Errors with the Credit Bureaus

The three major credit bureaus — Equifax, Experian, and TransUnion — maintain credit reports on almost all Americans with credit history. These reports include payment history, credit accounts, inquiries, and negative items. Lenders use these reports to decide whether to approve you and what interest rate to charge. Inaccurate information directly impacts your ability to borrow.

Dispute errors in writing, not by phone. Send certified mail with return receipt to prove you contacted the bureau. Include copies (not originals) of documentation supporting your dispute. The bureau must investigate within 30 days and report back. If they can't verify the accuracy of the error, they're required to remove it or correct it.

Some errors are creditor reporting mistakes, not bureau mistakes. If a creditor reported an account closed when it's open, or reported a late payment that didn't happen, dispute it with both the creditor and the bureau. The creditor must update their reporting within 15 days; the bureau must update within 30 days. Get both in writing.

Your credit report is free to check once yearly from AnnualCreditReport.com. Credit monitoring services cost extra ($10-15 monthly) but monitor your report automatically for changes and alert you to new accounts or inquiries. If you've had fraud or are a financial nervous person, it might be worth the cost. But the free annual report is sufficient if you check it carefully yearly.

Let 755CreditScore Handle Your Disputes

The DIY credit dispute process is straightforward but meticulous. First, get your free credit report from AnnualCreditReport.com. Second, identify inaccuracies — wrong balances, accounts that aren't yours, late payments you don't recognize. Third, write a dispute letter to the credit bureau with copies (never originals) of proof. Fourth, send certified mail with return receipt. Fifth, wait for their 30-day investigation.

What to dispute: accounts that aren't yours, wrong balances, late payments you don't recognize, accounts listed twice, closed accounts marked open. What not to dispute: accurate negative information (charge-offs, charge-off collections). Disputing accurate information wastes time — the bureau investigates, verifies it's accurate, and dismisses your dispute.

The proof you include matters. Dispute with documentation showing the creditor's error: bank statements proving you paid, letters from creditors confirming a payment, proof of payment from PayPal or bank transfers. Without documentation, the bureau will contact the creditor, they'll verify it's accurate, and your dispute is denied. Strong evidence gets faster, better results.

Sometimes DIY doesn't work — your dispute gets denied, or inaccuracies remain. This is when a credit repair professional becomes valuable. They know the system intimately, understand creditor-specific reporting quirks, and have relationships with bureau employees. A good credit repair professional handles cases DIY couldn't crack. But start with DIY first if you have the time and patience.